Daily Briefing – 20 giugno: negoziati USA-Iran in Svizzera, petrolio ancora volatile, ACHV ha la PDUFA di oggi, MU e FDX diventano i test della settimana, MRVL/FLEX entrano nel tratto finale S&P 500

Il briefing del 20 giugno per il sito .eu deve essere letto come aggiornamento weekend, non come seduta cash USA: oggi è sabato e Wall Street non è aperta. Le news fresche contano però eccome, perché preparano futures di domenica sera e riapertura del 22 giugno. Il centro del tape è cambiato rispetto al 19: la diplomazia USA-Iran torna in Svizzera, il petrolio resta volatile intorno al tema Hormuz, ACHV ha la sua PDUFA target date di oggi per cytisinicline, Micron diventa il test del rally AI il 24 giugno, FedEx darà una lettura sulla logistica/economia reale il 23 giugno, e MRVL/FLEX entrano nella finestra finale dell’inclusione S&P 500 prima dell’apertura di lunedì.

- Iran / Svizzera— La news geopolitica più fresca del 20 giugno è il ritorno dei negoziati in Svizzera: l’inviato USA Steve Witkoff e il ministro iraniano Abbas Araqchi sono diretti al Buergenstock per provare a trasformare l’intesa temporanea in un quadro regionale più ampio. Per il mercato non è un dettaglio diplomatico: oil, dollaro, difesa, travel e inflation trade restano legati alla credibilità di questo processo.Geopolitics

- Oil / Hormuz— Il petrolio resta il primo termometro macro del weekend. Dopo la riapertura parziale/normalizzazione dei flussi nello Strait of Hormuz, il mercato ha tolto parte del premio di guerra, ma la volatilità resta alta perché assicurazioni, transito navi, sicurezza e tempi della diplomazia possono cambiare rapidamente la lettura su Brent, WTI, airlines e energy equities.Oil Watch

- SPY / QQQ— Wall Street non ha una sessione cash oggi: il 20 giugno è sabato. La lettura corretta non è intraday, ma weekend/pre-Monday: il mercato deve decidere se il rally tech della settimana regge davanti a dollaro forte, Fed hawkish, oil volatility e nuovo ciclo di news sul Medio Oriente.US Reopen

- MU— Micron diventa il test più pulito della prossima settimana per capire se il rally AI può restare sostenuto. Gli investitori guardano agli earnings del 24 giugno come pulse check su HBM, memoria AI, data center demand, margini e capex. Se MU conferma domanda forte, il basket AI semis può restare in leadership; se delude, il mercato può iniziare a distinguere più duramente tra AI winners e AI expectations.AI Semis

- NVDA / AVGO / MRVL / AMD / ARM— Il basket AI semiconductor resta la parte più importante del tape growth. Nvidia guida la narrativa, Broadcom controlla custom silicon/networking, Marvell aggiunge index-flow e AI infrastructure, AMD misura il secondo livello del trade e Arm resta un proxy di architettura. La settimana prossima serve breadth, non solo headline.AI Basket

- MRVL / FLEX— Marvell e Flex sono ancora nel punto tecnico più importante: l’ingresso nello S&P 500 è previsto prima dell’apertura del 22 giugno. Il tema è meccanico ma reale: passive flows, ETF rebalancing, benchmark demand e possibili movimenti da sell-the-event dopo l’effettiva inclusione.Index Flow

- FDX— FedEx è il macro-earnings check del 23 giugno. Il mercato userà il call Q4 FY26 per leggere domanda logistica, industrial economy, pricing, cost control, trade flows e impatto dello spin-off FedEx Freight. Per chi guarda la salute dell’economia reale USA, FDX pesa più di quanto sembri.Earnings

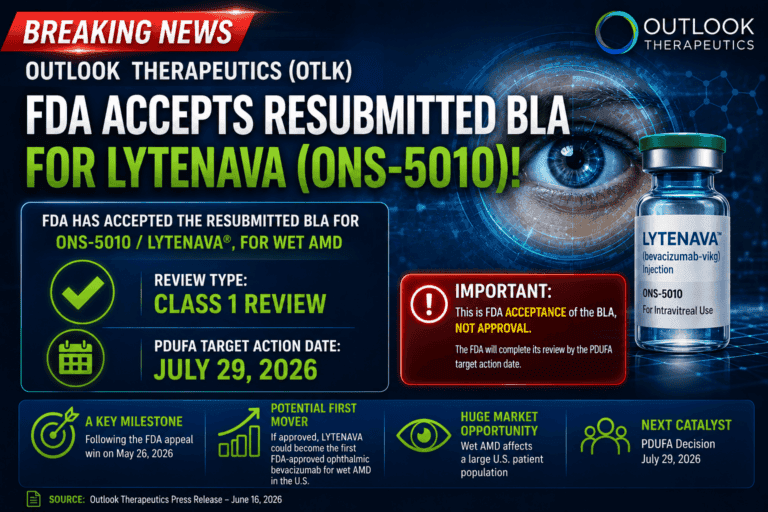

- ACHV— Achieve Life Sciences ha oggi, 20 giugno 2026, la PDUFA target date per cytisinicline nella smoking cessation. La lettura corretta è binaria ma prudente: finché non c’è comunicato FDA/company, non va trattata come approval. È però una delle scadenze biotech live del giorno.PDUFA Today

- SPRO / GSK— SPRO/GSK restano una notizia fresca da metabolizzare dopo l’approvazione FDA di Utebzi, tebipenem pivoxil, per adulti con complicated UTI inclusa pyelonephritis e opzioni orali limitate o assenti. La storia ora passa da rischio regolatorio a label, launch timing, stewardship, milestones e royalties.FDA Approval

- VRDN— Viridian resta il prossimo catalyst regolatorio pulito: veligrotug è sotto FDA Priority Review con PDUFA target date al 30 giugno 2026 per thyroid eye disease. Dopo SPRO e con ACHV live oggi, la biotech tape resta concentrata su date precise e outcome verificabili.PDUFA Watch

- ACN— Accenture resta il warning principale sull’AI services trade: la società ha riportato Q3 FY26 solido ma ha ristretto la guidance FY26 al 3%-4% in valuta locale. Il messaggio per il mercato è netto: AI infrastructure può correre, ma consulting e IT services non sono automaticamente beneficiari allo stesso ritmo.AI Services

- SPCX / RKLB / LUNR / PL— Lo space trade resta in fase di digestione dopo il grande momentum recente. SpaceX resta il termometro retail, ma lunedì la parte pubblica del paniere — Rocket Lab, Intuitive Machines, Planet Labs e altri proxy — dovrà mostrare forza relativa propria, non solo simpatia tematica.Space

- AAL / DAL / UAL / CCL / RCL— Travel e cruise restano legati al petrolio: un Brent meno stressato aiuta margini e sentiment, ma la diplomazia fragile sul Medio Oriente impedisce di trattare il calo del crude come fatto definitivo. Il trade funziona meglio se oil resta contenuto e il dollaro non diventa un freno eccessivo alla domanda globale.Travel

- XOM / CVX / SLB / ENI— Energy resta in bilico: meno premio di guerra pesa su upstream, ma qualsiasi intoppo su Hormuz, assicurazioni o negoziati può riportare supporto a oil majors e services. Per il sito .eu ha senso tenere anche ENI nel radar, perché la lettura mediterranea/energia resta diretta.Energy

- Weekend tape— Oggi non è una giornata di cash trading USA: è un briefing di sabato, quindi conta la preparazione alla riapertura di lunedì. Le notizie fresche vanno lette come input accumulati per futures di domenica sera e open del 22 giugno.Setup

- Fed / Dollaro— La Fed resta il freno silenzioso. Dollaro forte e lettura hawkish aumentano il costo del capitale e possono comprimere small caps, biotech speculative e long-duration growth. Il mercato può restare costruttivo, ma non è un risk-on senza condizioni.Rates

- PCE 25 giugno— Il prossimo macro gate è il PCE inflation del 25 giugno. Dopo il calo del petrolio e la nuova volatilità geopolitica, il dato diventa ancora più importante: un numero morbido aiuta risk assets; un numero caldo rafforza Fed hawkish e dollaro.Inflation

- Triple witching / Rebalance— La scadenza opzioni e i ribilanciamenti creano rumore tecnico. MRVL/FLEX, flussi ETF, volumi di chiusura e posizionamento possono distorcere i movimenti di breve periodo rispetto ai fondamentali.Flows

- Credit monitor— LQD e HYG restano segnali chiave. Un rally equity senza conferma del credito è più fragile; un credito stabile rende più credibile la continuazione del risk-on.Credit

- Europe read— Per l’Europa il mix è delicato: oil volatility sostiene energia e difesa, ma pesa su travel; healthcare resta difensivo; banche italiane e industriali dipendono da tassi, spread e rischio globale.Europe

Daily Briefing – June 20: U.S.–Iran Talks Move to Switzerland, Oil Remains Volatile, ACHV Has Today’s PDUFA Date, MU and FDX Become Next Week’s Tests, MRVL/FLEX Enter the Final S&P 500 Window

The June 20 briefing for the .eu site should be read as a weekend update, not as a U.S. cash-session note: today is Saturday and Wall Street is not open. Fresh news still matters because it sets up Sunday evening futures and the June 22 reopen. The center of the tape has changed from June 19: U.S.–Iran diplomacy is moving back to Switzerland, oil remains volatile around the Hormuz story, ACHV has its June 20 PDUFA target date for cytisinicline, Micron becomes the AI-rally test on June 24, FedEx will provide a logistics/real-economy read on June 23, and MRVL/FLEX are entering the final window before their S&P 500 additions become effective before Monday’s open.

- Iran / Switzerland— The freshest geopolitical story on June 20 is the return of Swiss diplomacy: U.S. envoy Steve Witkoff and Iranian Foreign Minister Abbas Araqchi are heading to Buergenstock to try to turn the temporary agreement into a broader regional framework. For markets, this is not just diplomacy; it directly affects oil, the dollar, defence, travel and inflation trades.Geopolitics

- Oil / Hormuz— Oil remains the weekend’s main macro thermometer. The market has removed part of the war premium after partial/ongoing normalization around the Strait of Hormuz, but volatility remains high because insurance, vessel traffic, security guarantees and the timing of diplomacy can quickly change the Brent/WTI, airlines and energy-equity read.Oil Watch

- SPY / QQQ— There is no U.S. cash session today because June 20 is Saturday. The right read is weekend/pre-Monday, not intraday: the market has to decide whether this week’s tech rebound can survive a strong dollar, a hawkish Fed, oil volatility and fresh Middle East headlines.US Reopen

- MU— Micron is the cleanest next-week test for whether the AI rally can stay supported. Investors are treating the June 24 earnings report as a pulse check on HBM, AI memory, data-center demand, margins and capex. If MU confirms strong demand, AI semis can keep leadership; if it disappoints, the market may start separating AI winners from AI expectations more aggressively.AI Semis

- NVDA / AVGO / MRVL / AMD / ARM— The AI semiconductor basket remains the core growth-leadership check. Nvidia anchors the narrative, Broadcom checks custom silicon/networking, Marvell adds index-flow plus AI infrastructure, AMD measures second-line appetite and Arm remains an architecture proxy. Next week needs breadth, not just headlines.AI Basket

- MRVL / FLEX— Marvell and Flex remain in their key technical window: their S&P 500 additions are scheduled before the June 22 open. This is mechanical but real: passive flows, ETF rebalancing, benchmark demand and potential sell-the-event behavior after the effective inclusion.Index Flow

- FDX— FedEx is the macro-earnings checkpoint on June 23. The market will use the Q4 FY26 call to read logistics demand, the industrial economy, pricing, cost control, trade flows and the FedEx Freight spin-off. For investors watching the real U.S. economy, FDX matters more than it looks.Earnings

- ACHV— Achieve Life Sciences has a June 20, 2026 PDUFA target date for cytisinicline in smoking cessation. The correct read is binary but cautious: until there is an FDA/company announcement, it should not be treated as an approval. It is, however, one of today’s live biotech catalyst dates.PDUFA Today

- SPRO / GSK— SPRO/GSK remain a fresh biotech story to digest after the FDA approval of Utebzi, tebipenem pivoxil, for adults with complicated UTIs including pyelonephritis and limited or no oral alternatives. The story has shifted from regulatory risk to label, launch timing, stewardship, milestones and royalties.FDA Approval

- VRDN— Viridian remains the next clean regulatory catalyst: veligrotug is under FDA Priority Review with a June 30, 2026 PDUFA target date in thyroid eye disease. After SPRO and with ACHV live today, the biotech tape remains focused on dated, verifiable outcomes.PDUFA Watch

- ACN— Accenture remains the key warning for the AI-services trade: Q3 FY26 was solid, but the company now expects FY26 revenue growth of 3%-4% in local currency. The market message is blunt: AI infrastructure can run, while consulting and IT services may not benefit at the same speed.AI Services

- SPCX / RKLB / LUNR / PL— The space trade remains in digestion mode after the recent momentum wave. SpaceX remains the retail thermometer, but the public basket — Rocket Lab, Intuitive Machines, Planet Labs and other proxies — needs its own relative strength on Monday, not just theme sympathy.Space

- AAL / DAL / UAL / CCL / RCL— Travel and cruises remain tied to oil. Lower-stress Brent helps margins and sentiment, but fragile Middle East diplomacy means the crude decline cannot be treated as a settled fact. The trade works best if oil stays contained and the dollar does not become too heavy a demand headwind.Travel

- XOM / CVX / SLB / ENI— Energy remains balanced between lower war premium and renewed headline risk. Any problem around Hormuz, insurance or negotiations can support oil majors and services again. For the .eu site, ENI also belongs in the radar because the Mediterranean/energy read is direct.Energy

- Weekend tape— Today is not a U.S. cash-trading day; it is a Saturday briefing. Fresh headlines should be read as inputs for Sunday evening futures and the June 22 open.Setup

- Fed / Dollar— The Fed remains the quiet brake. A strong dollar and hawkish policy read raise the cost of capital and can compress small caps, speculative biotech and long-duration growth. The market can stay constructive, but this is not unconditional risk-on.Rates

- PCE June 25— The next macro gate is the June 25 PCE inflation release. After lower oil and renewed geopolitical volatility, the number matters even more: a soft print helps risk assets; a hot print reinforces the hawkish Fed and the dollar.Inflation

- Triple witching / Rebalance— Options expiration and index rebalancing create technical noise. MRVL/FLEX, ETF flows, closing volumes and positioning can distort short-term moves versus fundamentals.Flows

- Credit monitor— LQD and HYG remain key confirmation signals. An equity rally without credit support is more fragile; stable credit makes risk-on more credible.Credit

- Europe read— For Europe the mix is delicate: oil volatility supports energy and defence but weighs on travel; healthcare stays defensive; Italian banks and industrials depend on rates, spreads and global risk.Europe